You may have noticed that, over the last two years, it seems that cyberattacks are on a steep rise. If so, you aren’t wrong. In the first half of 2021 alone, there was a 1,318% year-on-year increase in ransomware attacks on banks. And if you work in a financial organization, your chances of experiencing a cyberattack are 300 times higher than in other sectors.

The link between cyberattacks and financial institutions isn’t inconsequential. There is a strong correlation between the increase in these attacks and those in the finance sector.

In this post, we’re going to be looking at why this correlation exists as well as what institutions can do about it.

What data do financial service organizations house?

For the most part, cyberattacks are specifically targeting data. So, to understand why this negative relationship is here, it’s important to examine the data that financial services house.

Finances and spending habits

The first segment of data that these organizations store is tied to individuals’ finances and spending habits. By extorting the data that banks and other institutions hold, bad actors can gain personal insights into how much money people have and how they’re spending it.

While this can be a concern for anyone, especially in the case of stolen identities, it can be a major concern for persons of interest and public figures. This information can be used to harm reputations, plan future attacks, and commit fraud.

Social media and online payments

Financial organizations also have access to the social media activity of their customers and the online transactions that they’re making.

That’s because financial services invest in tracking the websites and physical areas that their customers spend time in to verify their identities. And, of course, every online transaction that a customer makes is recorded by their bank of choice.

Again, these connections can be exploited by bad actors to gain information on potential victims.

Credit card and social security numbers

Lastly, banks and other organizations store credit card numbers and social security information. Credit card numbers can be used to make fraudulent purchases, sometimes going completely unnoticed for days or even weeks if the attack is subtle.

Social security numbers, on the other hand, can be used to gain access to a person’s identity, leading to identity theft and similar crimes.

Do they know they need to be protecting this data?

Unfortunately, this data isn’t the only reason that financial organizations have become a key target for cyberattacks. Another factor in this rising threat is the fact that members of these organizations aren’t even aware that they need to be actively protecting this data.

In fact, a third of financial institutions surveyed said they lacked a clear roadmap for addressing privacy and security risks.

Oftentimes, staff members assume that there are strong enough systems in place to prevent the exploitation of data from ever occurring. Little do they know that, more often than not, the weakest link in a business’s security system is the staff itself.

This is why education and training are crucial. Your staff can play a key role in preventing cyberattacks from taking place, so long as they aren’t kept in the dark.

The importance of compliance

While it is true that many employees of financial institutions don’t know the extent to which they should be protecting customer data, this does not mean that there are not rigid guidelines in place to keep data safe. There are a few sets of guidelines that financial institutions must ensure they are compliant with.

PCI-DSS

The Payment Card Industry Data Security Standard (PCI-DSS) is an international standard that protects cardholders’ data from misuse or theft. Organizations handling payment card transactions must remain compliant with this standard in order to continue operating.

This involves tracking and monitoring all access to network and cardholder details, regularly testing and optimizing security systems, securing audit trails, employing file integrity monitoring, and performing weekly critical file comparisons.

GDPR

The General Data Protection Regulation (GDPR) is Europe’s unified data protection framework which applies to any EU or non-EU organization processing the personal data of individuals based in the EU. Again, compliance is mandatory for continued operation.

NIS2

The NIS2 directive builds on previous EU requirements to protect critical infrastructure and organizations within the EU from cyber threats. Mandatory for all supply chains across the EU, all member states are expected to comply by 2024.

The NIS2 directive hopes to achieve higher levels of data security by providing total coverage and communication across supply chains, requiring compulsory incident reporting, and setting out a security standard to be adhered to. You can download a complete guide to NIS2 here.

Are financial organizations ready to protect this data?

The answer to this question is both “Yes” and “No”. Yes, banks are aware of the growing threat of cyberattacks and are investing in security systems. But also, no, many of them aren’t doing enough for a variety of reasons. Here is a quick breakdown of some of the reasons that financial services are falling short when it comes to cybersecurity.

Lack of training and budget

First, many organizations lack the training and the budget to adequately defend themselves against modern cyberattacks.

Budgetary shortcomings make it challenging for organizations to invest in the latest solutions to combat the latest attack methods. Cyber risk is a business risk.

For a variety of reasons, budget chief among them, they aren’t spending time training their staff on the role they play in protecting their organization. Combined, these two factors lead to a poor defense.

Lack of specialists

Another reason that financial institutions are falling behind in the fight against cybercrime is that they lack specialists. As we’ll discuss below, cyberattacks are becoming more sophisticated, and as a result so too must the response to them. Specialists are required, who need to be on call at all times ready to stop, mitigate, and repair incoming threats.

This talent can be difficult and expensive to acquire, leaving banks without the protection they need to stand firm against these attacks.

Cyberattacks are becoming more sophisticated

Lastly, there is the simple fact that cyberattacks are becoming increasingly sophisticated. Each year, and sometimes every few months, there is a new type of attack that banks need to be prepared for.

And, as we’ve covered, most institutions simply don’t have the resources, staff, or training to be able to combat these incoming attacks. Hackers are innovating faster than most institutions can keep up with.

Difficulties with compliance

Despite the fact that regulations such as PCI-DSS and GDPR are in place and mandatory, many institutions have difficulties in achieving compliance. This is due to the strict requirements, the time-consuming nature of the guidelines, and a lack of robust security tools present in many financial organizations.

It is crucial that organizations implement a solution like BCS for SAP, as SAP systems are a significant part of the economy and commerce. GDPR and BCS for SAP work together to protect customer data, and without full compliance with all regulations, financial institutions not only face legal action and fines but also leave data open to exploitation.

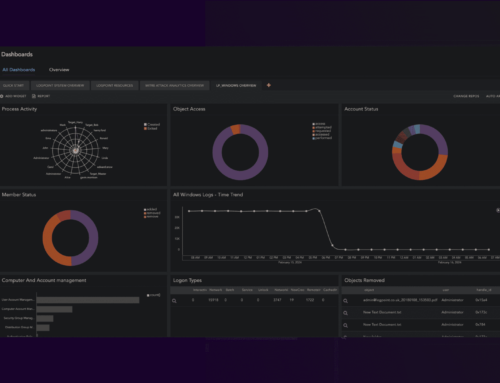

How Logpoint helps institutions secure their data

Fortunately, financial institutions don’t have to face these threats alone. Logpoint has a variety of cloud-based and on-premises solutions available to help protect your financial institution.

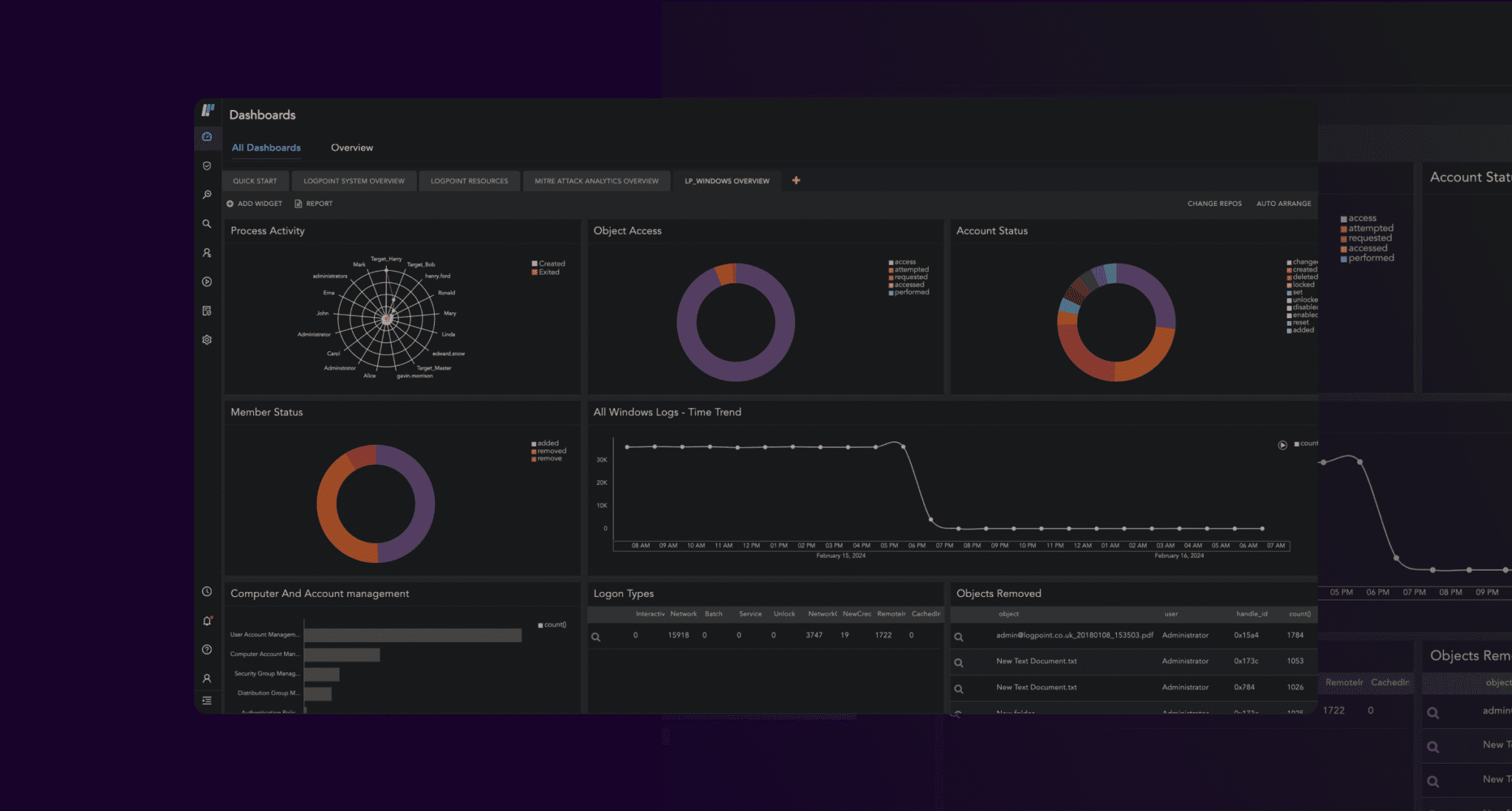

Logpoint developed our converged SIEM platform to instantly detect when a potential threat is incoming. The threat is then flagged, verified, and brought to the attention of your IT team.

Additionally, Logpoint has tools in place that allow your organization to monitor your users’ activity. Whether you’re looking at internal use cases or customer use cases, our software can help keep your firm safe.

And as an EAL 3+ certified provider, you can be confident that you are receiving the highest standard of protection on the market.

For more information, take a tour of our solution, or book a demo with Logpoint today.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}